The Underground Energy Transition

Part 1 — The Drilling Constraint

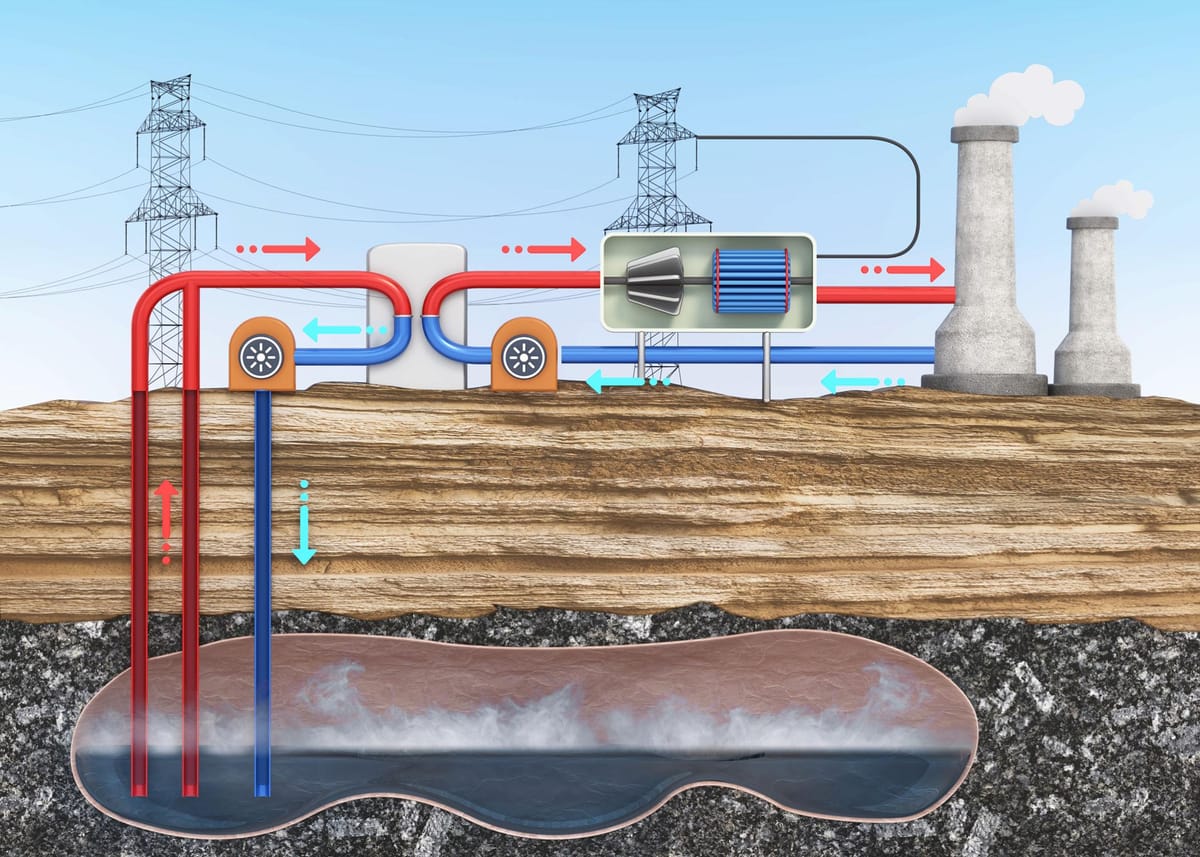

Why Geothermal, CCS, and Hydrogen All Compete for Drilling Capacity

When people talk about the energy transition, the focus usually falls on visible technologies.

Wind turbines.

Solar panels.

Battery storage.

But a growing part of the energy system will depend on something far less visible.

The ground beneath our feet.

Geothermal energy, carbon storage, and hydrogen storage all rely on one fundamental capability:

The ability to drill deep wells safely and reliably.

The Illusion of Speed

Renewable deployment often appears fast.

Solar farms can be installed in months.

Wind turbines can be erected in weeks.

But subsurface energy infrastructure moves at a very different pace.

Every geothermal system, carbon storage project, or hydrogen cavern requires wells drilled thousands of meters underground.

Those wells are complex industrial projects.

They require drilling rigs, specialized crews, and extensive subsurface analysis.

Unlike surface technologies, they cannot be mass-produced in factories.

They must be engineered well by well.

The Subsurface Demand Explosion

Several major energy technologies now depend on the same underlying capability.

Deep drilling.

Geothermal development requires wells that reach high-temperature reservoirs several kilometers underground.

Carbon capture and storage requires injection wells capable of safely storing CO₂ in deep geological formations.

Hydrogen storage relies on underground caverns or depleted reservoirs that must be drilled and engineered.

In other words, three different sectors of the energy transition are beginning to compete for the same industrial resource.

At the same time, investment in geothermal development is accelerating as governments and private capital rediscover its potential as a reliable energy source.

Subsurface engineering capacity.

The Rig Constraint

The global drilling fleet has shrunk significantly over the past decade.

Many of the companies with the expertise required to drill these wells were built in the oil and gas industry.

As oil and gas investment cycles slowed and many offshore fields matured, rigs were retired and service companies consolidated.

Yet the emerging subsurface energy industries are moving in the opposite direction.

They require more wells, not fewer.

Which creates a structural mismatch.

We are planning a 2030 energy system with a 1990s drilling fleet.

The Lead-Time Reality

Drilling capacity cannot be expanded overnight.

Bringing new rigs into operation, refurbishing existing fleets, and training specialized crews typically requires 24 to 36 months.

Rigs must be reactivated.

Crews must be upskilled.

Supply chains for high-temperature alloys and drilling tools must be rebuilt.

These are not software updates.

They are physical deployments.

Even if policymakers decided tomorrow to accelerate geothermal, CCS, and hydrogen storage simultaneously, the industrial capacity to drill the required wells would lag years behind the ambition.

Strategic Implication

The energy transition is often framed as a technology race.

But it may also be an industrial capacity problem.

In many regions the geothermal resource is not the limiting factor.

The ability to drill and manage wells at scale is.

Because while wind turbines and solar panels capture the imagination, a large part of the future energy system will depend on what happens deep underground.

And underground infrastructure is built slowly, one well at a time.

Suggested LinkedIn Caption

The energy transition is often framed around visible technologies - wind, solar, batteries.

But geothermal energy, carbon storage, and hydrogen storage all rely on something much less visible.

Drilling capacity.

As subsurface energy technologies expand, they are beginning to compete for the same rigs, crews, and engineering expertise.

That raises an interesting question:

Are we planning a 2030 energy system with a 1990s drilling fleet?

Comments ()